Critical Minerals

The Backbone of the Clean Energy Transition

BLOG POSTS

Amal Ismail

The global shift towards clean energy sources is accelerating, driven by international efforts to reduce carbon emissions and achieve the goals of the Paris Agreement. Critical minerals play a pivotal role in this transition, as they are essential components in manufacturing renewable energy technologies such as solar panels, wind turbines, electric vehicles (EVs), energy storage systems(BESS), and electrolyzers for Hydrogen production. However, the increasing demand for these minerals raises new challenges related to mineral security and environmental and social sustainability.

Escalating Demand Driven by Clean Energy Technologies

The production of many critical minerals is concentrated in a limited number of countries and is primarily fueled by the rapid deployment of clean energy technologies. According to the latest data from the International Energy Agency (IEA), in 2023, lithium demand soared by 30%, while nickel, cobalt, graphite, and rare earth elements experienced growth rates between 8% and 15%. Electric vehicles (EVs) have emerged as the predominant consumers of lithium, substantially increasing their share in the demand for nickel, cobalt, and graphite.

Projections indicate that if countries fulfill their announced energy and climate targets, the demand for minerals in clean energy technologies could be more than double by 2030 and triple by 2040, reaching nearly 35 million tons annually.

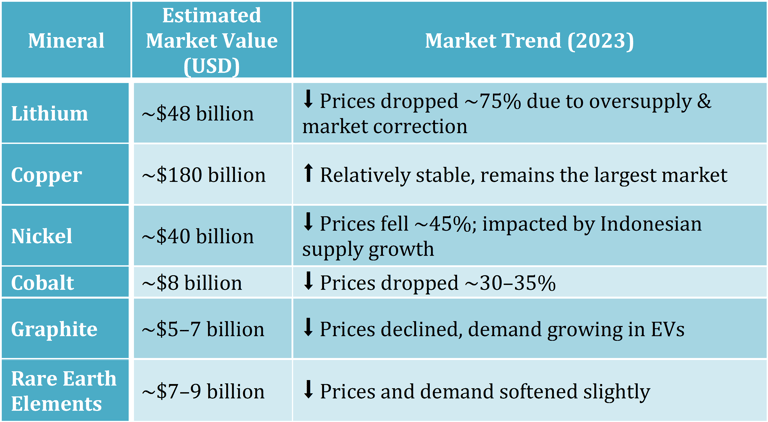

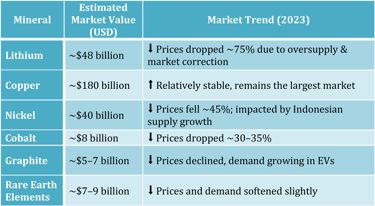

Market Value of Key Energy Transition Minerals

The total market size for energy transition minerals was ~$325 billion in 20233 —, down 10% from 2022 due to significant price drops. Despite falling prices, volumes traded increased, showing underlying demand growth. Copper remains the largest single market, followed by lithium and nickel. Market volatility is expected to continue due to supply-demand imbalances, policy shifts, and global economic trends.

Source: IEA’s Global Critical Minerals Outlook 2024

Table (1): Market Value of Key Energy Transition Minerals 2023

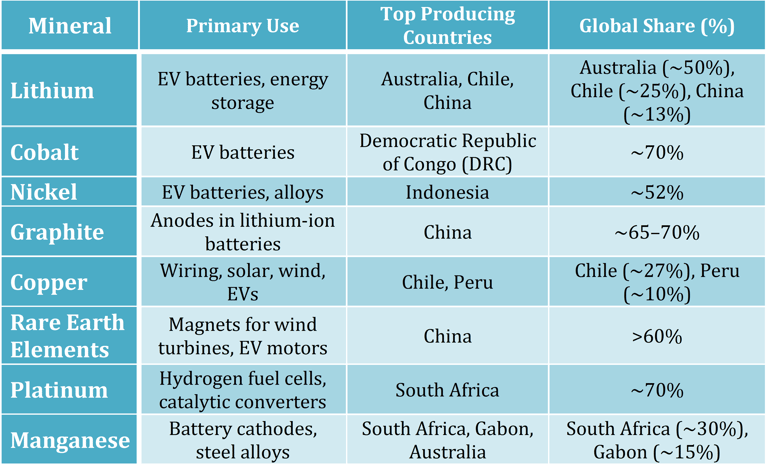

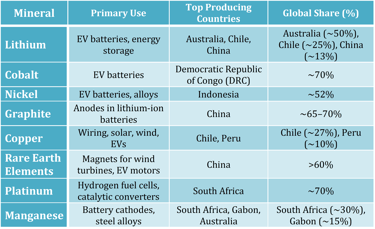

Supply Chain Concentration

The supply chains for critical minerals are increasingly concentrated geographically, posing potential risks to global energy security. For example, Indonesia's share of mined nickel production rose from 34% in 2020 to 52% in 2023, and its share of refined nickel increased from 23% to 37%. China dominates processing and refining for many of these minerals, even when mining takes place elsewhere. Such concentration heightens the vulnerability of supply chains to geopolitical tensions, trade restrictions, and other disruptions. So there is a need for diversified and resilient supply chains to mitigate these risks.

Source: IEA’s Global Critical Minerals Outlook 2024

Table (2): Top Producing Countries of Key Critical Minerals (2023)

Environmental and Social Considerations

The extraction and processing of critical minerals often entail significant environmental and social challenges. Mining operations can lead to habitat destruction, water and air pollution, and adverse impacts on local communities. Moreover, refining processes, particularly in regions reliant on coal-based electricity, contribute to high carbon emissions.

Addressing these concerns necessitates the adoption of sustainable and responsible practices across the mineral supply chain to protect the environment, workers, and communities, ensuring that the benefits of mineral development are equitably shared.

Conclusion

In the process of transitioning to clean energy, critical minerals pose new challenges to energy security. Minerals are central to all technologies associated with clean energy, whether for energy production or storage. With China's global dominance in critical minerals, regional countries are pushing to secure supply chains and strengthen partnerships with producing countries such as Australia and South America.

For Egypt and the MENA Region, the shift towards clean energy represents a significant opportunity to play a global role in securing supply chains and developing sustainable energy technologies. However, success in this transition depends on investing in infrastructure, enhancing local capacity in mining and manufacturing, exploiting regional mineral resources, and building capabilities in energy technology manufacturing to reduce reliance on imports and achieve energy independence while adapting to global changes in demand for critical resources and minerals.

References

Address

No 10, Block 28023

3rd District, Obour City, Egypt

Contacts

+201100899991

Careers

Copyright © EUMENA 2024

Terms and conditions

Privacy Policy

Commercial Reg.

105282